The current fiscal year budget has an $18 million deficit, which must be covered by university reserves. This use of reserves will deplete the E&G reserve balance to a level below the minimum threshold established by policy.

The Reserves Shell Game

So the need to slash $18 million from current service levels (CSL) by the start of the next fiscal year is premised on this unavailability of reserve funds. Of course, the Board of Trustees could make an exception to their policy of not spending below the minimum threshold, as they did for the current fiscal year. We’re told they won’t.

The administration did actually have a plan to run an E&G budget deficit through 2025-26, further drawing down E&G reserves by $8 million, after which budget surpluses would allow rebuilding the reserves starting in 2026-27. (See F&A Committee slidedeck, 4 April 2024, pp. 41-42.) Nevertheless, and despite ending the past year with $6.4 million more in reserves than anticipated when the Board approved the reserve spend in June, “program revitalization” has been re-envisioned to require a balanced budget a year early.

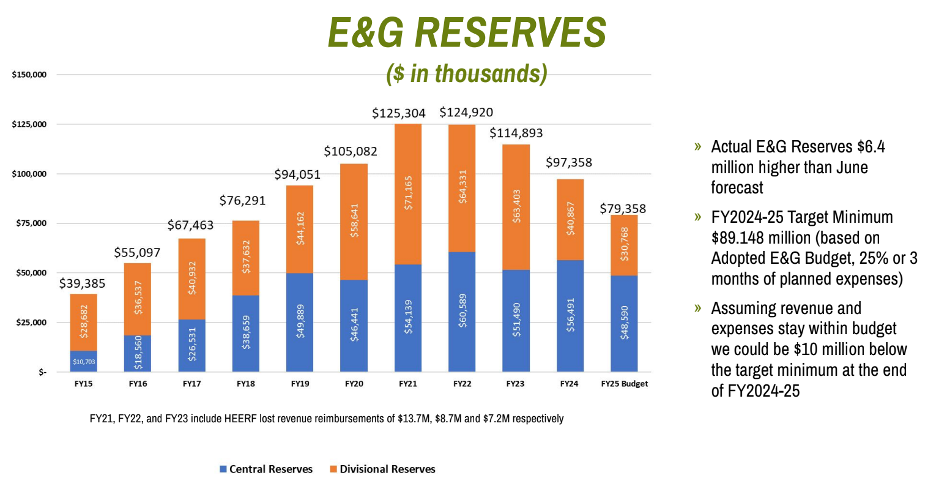

Even setting aside the question of why the Board is now, apparently, unwilling to tap reserves beyond this year, we should ask: How much money does the university have in reserves? If you have observed meetings of the Board of Trustees, you have seen iterations of this chart of E&G reserves over time (Board of Trustees slidedeck, 27 September 2024, p. 32):

The university does have other non-E&G reserve balances, each with minimum thresholds established by policy. Together these amounted to $88 million at the end of last year. All of these reserve funds are above their minimums, except for Treasury reserves, which is slightly below. (See F&A Committee slidedeck, 26 September 2024, p. 28). If there are excess non-E&G reserves, why aren't they being discussed by the Board as a supplement to E&G reserves?

The Pretend Pension Liability

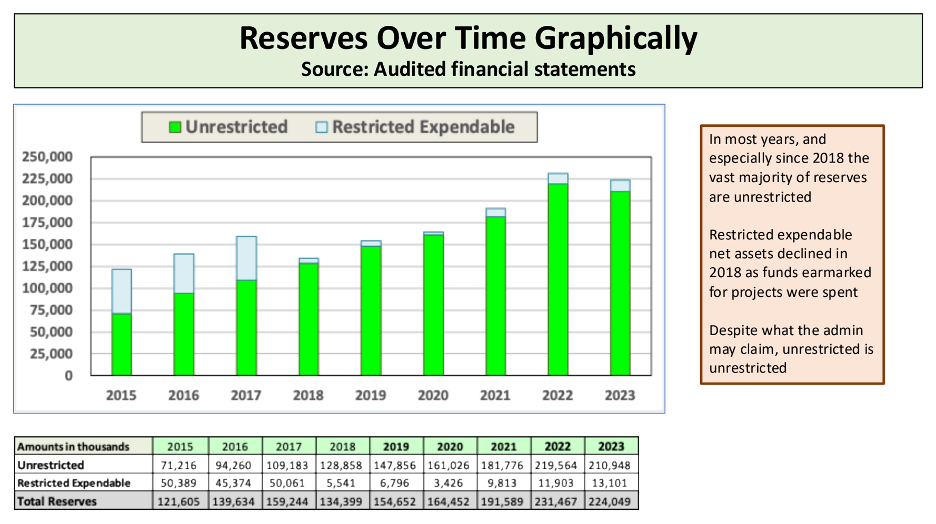

Now, if you’ve looked over the Financial Analysis by Howard Bunsis, you have seen this chart (p. 15). Bunsis’s analysis is based on PSU’s audited financial statements. The financial statement for the fiscal year ending in 2024 is not yet available, but just looking at 2023, there is a big difference between the PSU administration’s $115 million in E&G reserves (above) and what Bunsis reports as $211 million in “unrestricted” reserves (below).

As stated in the university’s 2023 Financial Report, “unrestricted are resources that may be used at the discretion of the Board” (p. 37). But Bunsis’s figure is substantially greater than the $61.6 million shown in the Report. Why? Because he makes an adjustment for pension liabilities. Bunsis points out that $149.3 million of liabilities on the university's balance sheet are there only for accounting purposes. They do not actually diminish the reserve funds expendable by the Board. You add that back in and it comes to $211 million in reserves.

A change in accounting practices required public universities to include pension obligations on their balance sheets; in 2018, retiree healthcare obligations were added to public university balance sheets for the first time. These changes are commonly referenced as GASBs 68 and 75 (for Governmental Accounting Standards Board). However, pensions and retiree healthcare benefits are fundamentally obligations of the State of Oregon, not the university itself. Bond-rating agencies, such as Moody's, understand the nature of these obligations. As a result, they make adjustments in their analyses for all public universities, recognizing that these liabilities are ultimately the responsibility of the state rather than the individual institutions.

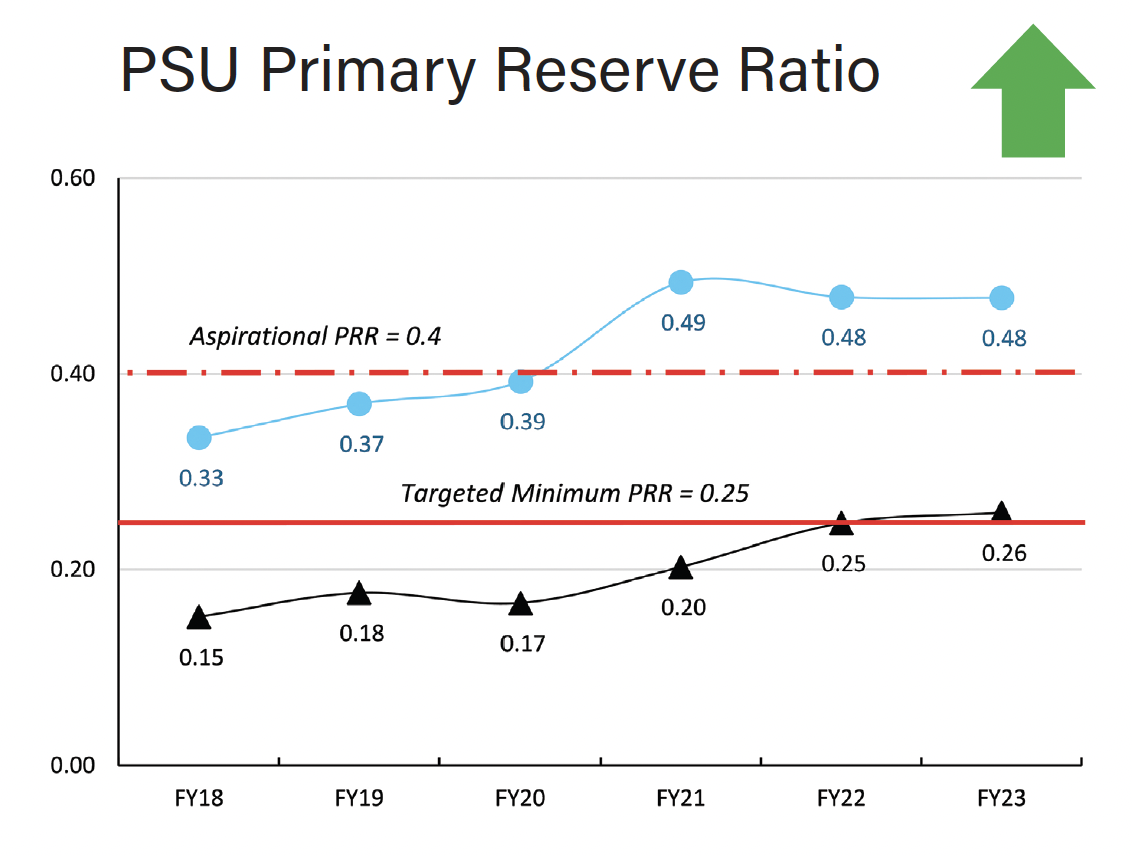

PSU also finds it useful to report reserves with and without the retirement-related liabilities identified in GASBs 68 and 75. The primary reserve ratio, as the University states, is the ratio of “expendable net assets, over the institution’s (including its affiliated foundation) total operating expenses.” Again, according to Board policy, the reserve ratio should be above 25% of operating expenses (90 days). As we see from PSU’s Financial Profile (p. 21), university reserves – E&G and non-E&G – were above that minimum in 2023 (black line with triangles). When retirement-related liabilities are separated out, reserves are at 48% of expenses (blue line with circles) – which is well above even the Board’s “aspirational” level of 40%.

When the administration wants to trumpet its sound financial management, it likes to draw attention to this alternative calculation of PSU’s reserve balance excluding these liabilities. But when they want to emphasize budgetary strain, they report reserve fund balances, inclusive of these liabilities. The E&G reserve cash balance in 2023 was $155 million, or $40 million more than shown in the administration’s E&G reserve chart above, which was prepared for the Board meeting in September (Financial Profile, p. 13; the 2023 amount is the most recent available).

What’s the Point of Strategic Planning?

The University has the resources and Board of Trustees has the discretion to allow the administration to take a more deliberate approach to program revitalization. Strategic planning is a waste of time and effort, not to mention untold consultancy fees, if no opportunity is afforded to operationalize the plan in a considered way. Instead – and yet again – academic units have been handed their budget targets as our campus community suffers another blow to employee morale.